Through the Fog: Risk and Opportunities Abound

Highlights

We believe:

- The U.S. economy remains on solid footing, though growth has moderated. GDP growth is now expected at 2.5%, with labor, productivity, and both economic sectors expanding to extend the current cycle.

- Corporate earnings are the engine driving this bull market higher. Six consecutive quarters of double-digit growth and rising analyst estimates have led us to raise our S&P 500 year-end target from 7700 to 8100.

- Investor pessimism remains a contrarian positive for equities. With bearish sentiment near historic extremes and $7.9 trillion sitting in money market funds, abundant dry powder could cushion corrections and fuel future gains.

- The Fed is in a prolonged holding pattern, but the risk has shifted toward rate hikes. Inflation accelerated on the back of the Iran conflict, though declining oil prices from their April peak may reduce pressure on the Fed to act.

- Midterm election year volatility is a risk to manage, not a reason to exit. History shows sharp corrections in midterm years are typically followed by exceptional recoveries, and we would view any pullbacks as buying opportunities given the strong fundamental backdrop.

Coming into this year, we expected the market to push further into new-high territory and the economy to continue its expansion with solid growth. We expected the economy to grow 3.0% with the combination of fiscal and monetary stimulus set for 2026. The economy is on solid footing, but likely to grow a bit slower due to the rising energy costs. We now expect 2.5% GDP growth.

There were many bullish trends that supported the market including a “wall of worry”, a dovish Fed, record corporate earnings, and disinflation. The Fed is no longer outright dovish but likely on an extended pause, and inflation is creeping higher. Our year-end target for the S&P 500 was a bullish 7700 with corporate earnings the primary driver of stock prices this year. Forward earnings continue to accelerate and lift our year-end S&P 500 target to 8100. The market’s sharp rebound has it on the way to a fourth consecutive double-digit year.

Risks to the outlook are many, including a new Federal Reserve Chair and midterm elections, both of which historically contribute to volatility and sizable corrections. In addition, concerns over private credit funds gating withdraws, the AI capital spending spree and bond issuance, and geopolitics continue to weigh on investor minds. A war in Iran wasn’t on our bingo card, but the market rebounded strongly after an initial mild drawdown as expected per historical precedent.

The Economy Expands Despite Energy Pressures

The U.S. economy has been extraordinarily resilient in the face of tariffs, inflation pressures, and the war in Iran. Economic activity is out to a new high; real GDP grew by 2.0% last year and rose by 1.6% in the first quarter. The Atlanta Fed GDPNow forecast is tracking 2.8% for the second quarter.

We had initially expected 3.0% real growth this year, but headwinds from higher energy costs and interest rates have led us to lower our GDP growth expectation to 2.5%. Unfortunately, the K-shaped economy has those at the bottom feeling the strain of higher energy costs, inflation, and declining real wages. Those at the top of the K and asset owners are doing much better.

Despite the headwinds from geopolitical concerns, domestic production continues to move ahead, with both the manufacturing and service sectors expanding. The labor market is solid and growing again after a brief slowdown, and the economy is benefiting from a productivity boom and AI capex spending. The U.S. economy has been less impacted than other developed economies from higher oil costs. This all puts the U.S. in a strong competitive global position. (See Figure 1.)

Figure 1

Perspective

Source: Bloomberg

Past performance is not indicative of future results. This is not a recommendation to buy or sell a particular security. Please see disclosures at the end of this document.

As it stands today, the economy employs a record 159 million people. After a period of some softness, the labor market has been a little firmer in recent months. Payroll growth has surprised to the upside with improving breadth, and job openings have rebounded. Over the last three months the economy added an average of 188,000 jobs per month (compared to only 10,000 jobs added per monthbfor all of 2025). The unemployment rate is only 4.3%, which is a little below the Fed’s Summary of Economic Projections estimate.

Over the past several years, we have said a recession is not in the cards unless there is meaningful weakness in the labor market. For the Fed, a slightly stronger labor market means less downside risk, so policy can focus on inflation.

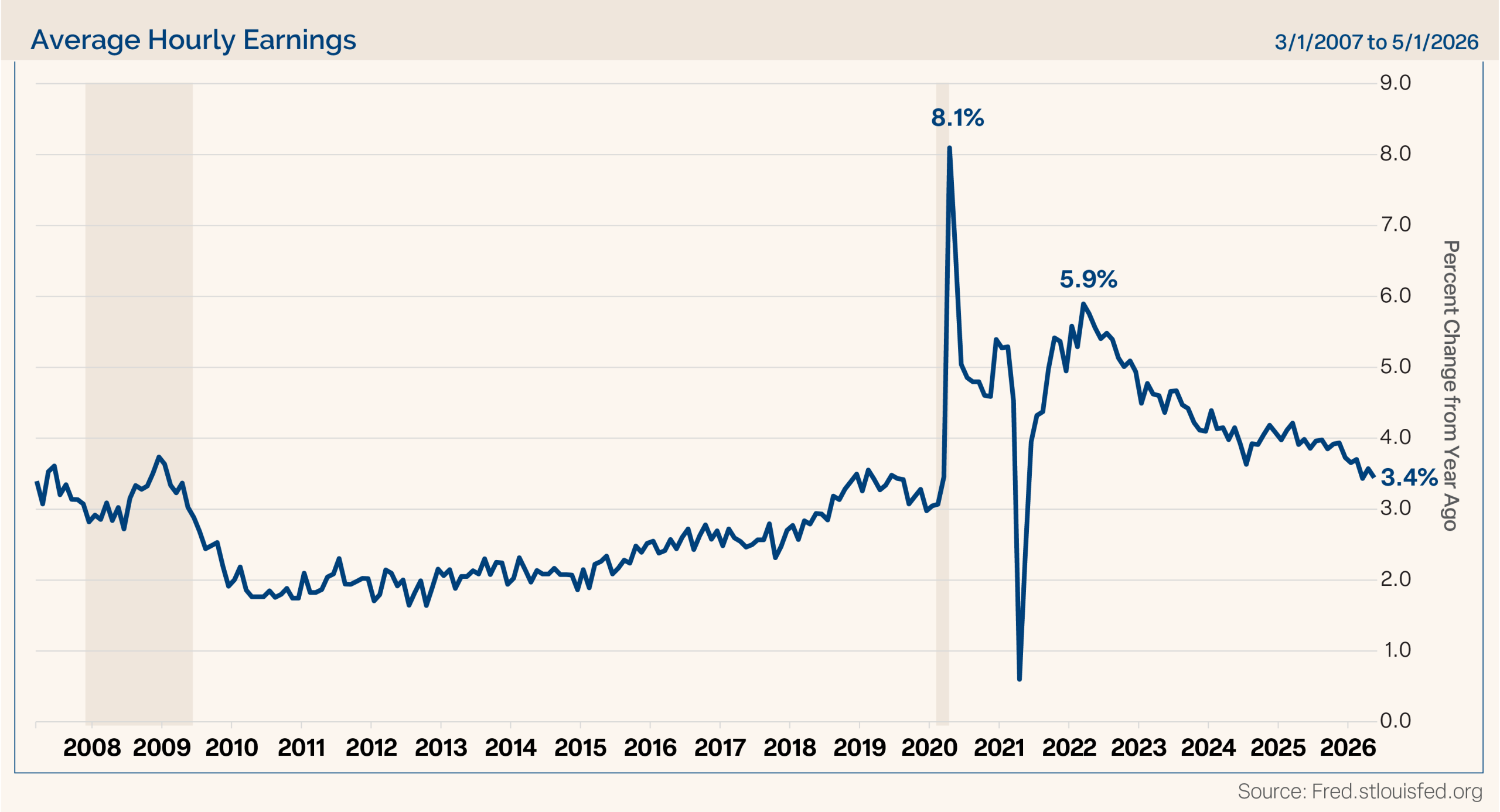

We still see the labor market as a source of disinflation, with unit labor costs (wages minus productivity) only growing in the low 1% range. In addition, average hourly earnings have been trending lower over the past couple of years. (See Figure 2.) At 3.4%, earnings are not keeping pace with inflation, so many workers are experiencing a loss of purchasing power in real terms.

Figure 2

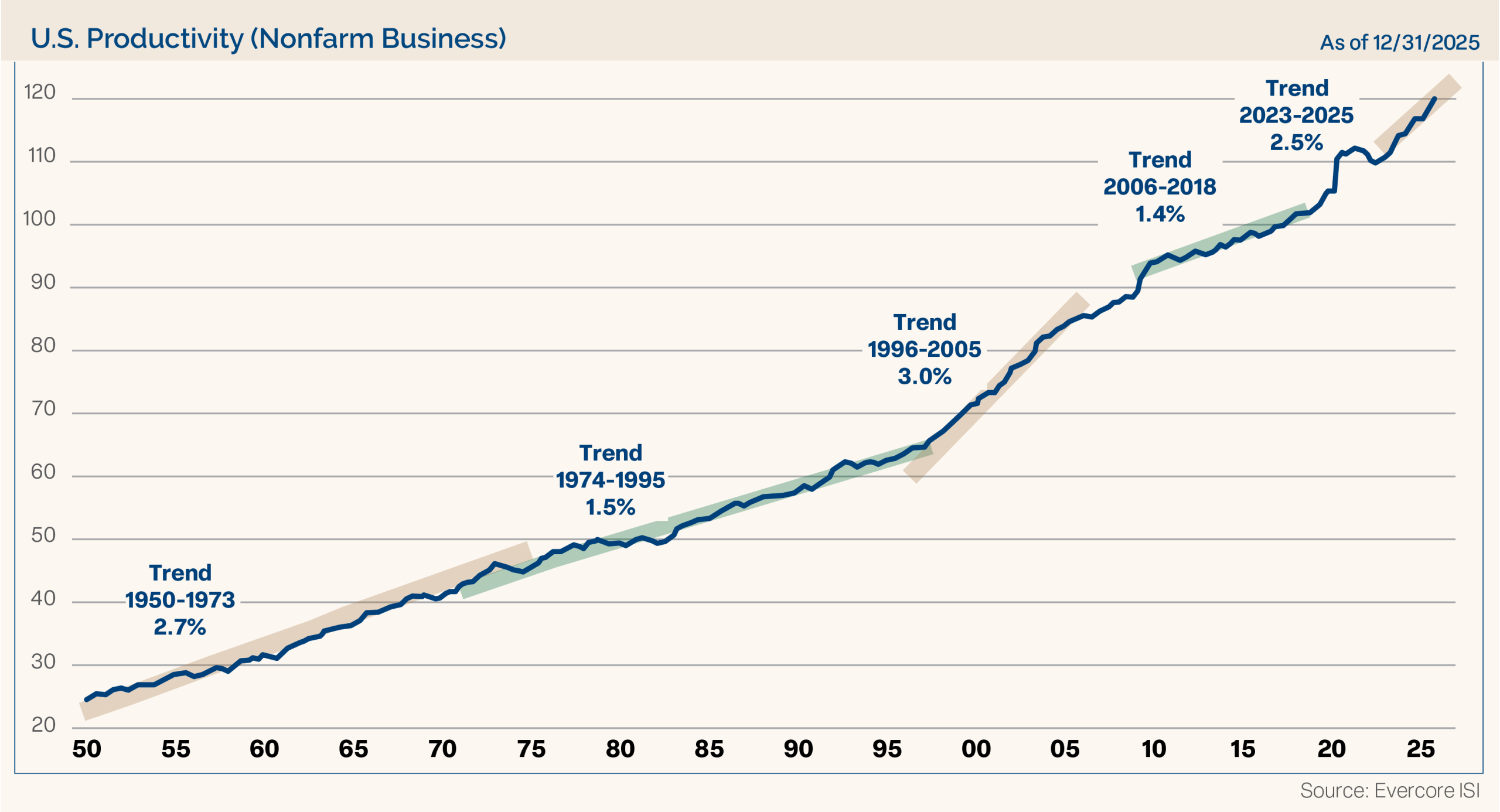

Productivity has surged since the COVID lows, and interestingly, productivity tends to surge for decades at a time. (See Figure 3.) Productivity increased 2.8% annually in the fourth quarter of 2025 and has averaged 2.5% since 2023. AI should continue to power that trend. Strong productivity should extend the shelf life of the current economic cycle, as it did in previous periods.

Figure 3

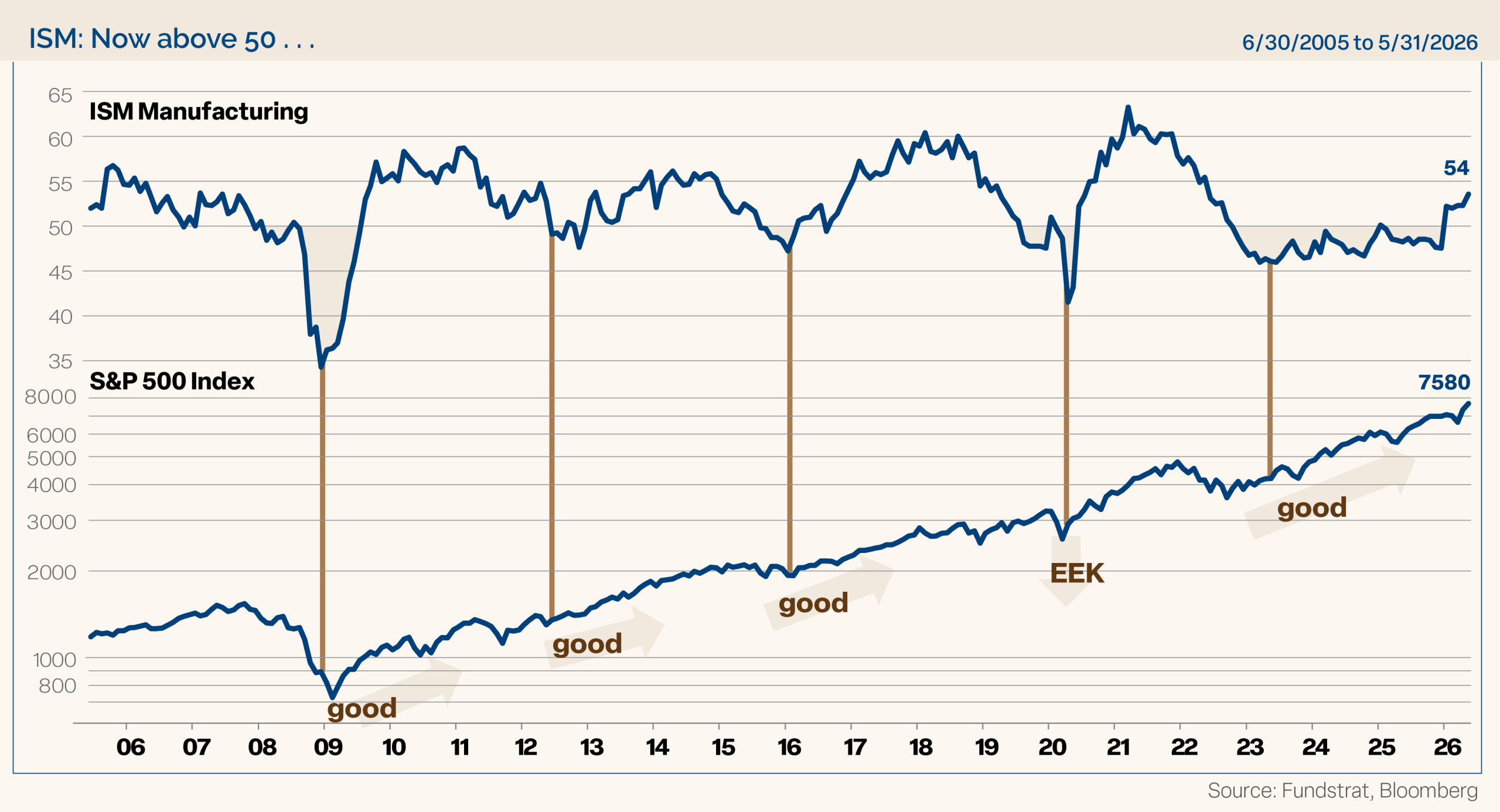

The Institute for Supply Management (ISM) Manufacturing Index had been in the contraction zone below 50 for 35 of the last 37 months through December 2025, the longest stretch of time it had been in contraction since its inception. Even during the global financial crisis (GFC), it was only in contraction for a 16-month period.

In our Annual Outlook we stated, “Given the expectation of both fiscal and monetary stimulus, continued economic growth and AI buildout, we expect the manufacturing sector to enter expansion territory in early 2026.” It returned to expansion territory in January and has been expanding for five straight months.

Now both sectors of the economy, manufacturing and service, are expanding. Purchasing Managers’ Indices (PMI) rose to their highest level since mid-2022, new orders and production picked up, and inventories are low, likely signaling future production. On the service side, 17 of 18 industries reported growth. Only real estate contracted, as it is plagued by higher lending costs.

The market historically performs well from the depth of the manufacturing sector contraction until well into expansion territory and starts to turn down near late cycle expansions. (See Figure 4.) So far this cycle, the ISM Manufacturing Index bottomed in March 2023, and the S&P 500 has advanced 91% since.

Figure 4

Navigating Potential Corrections in a Midterm Election Year

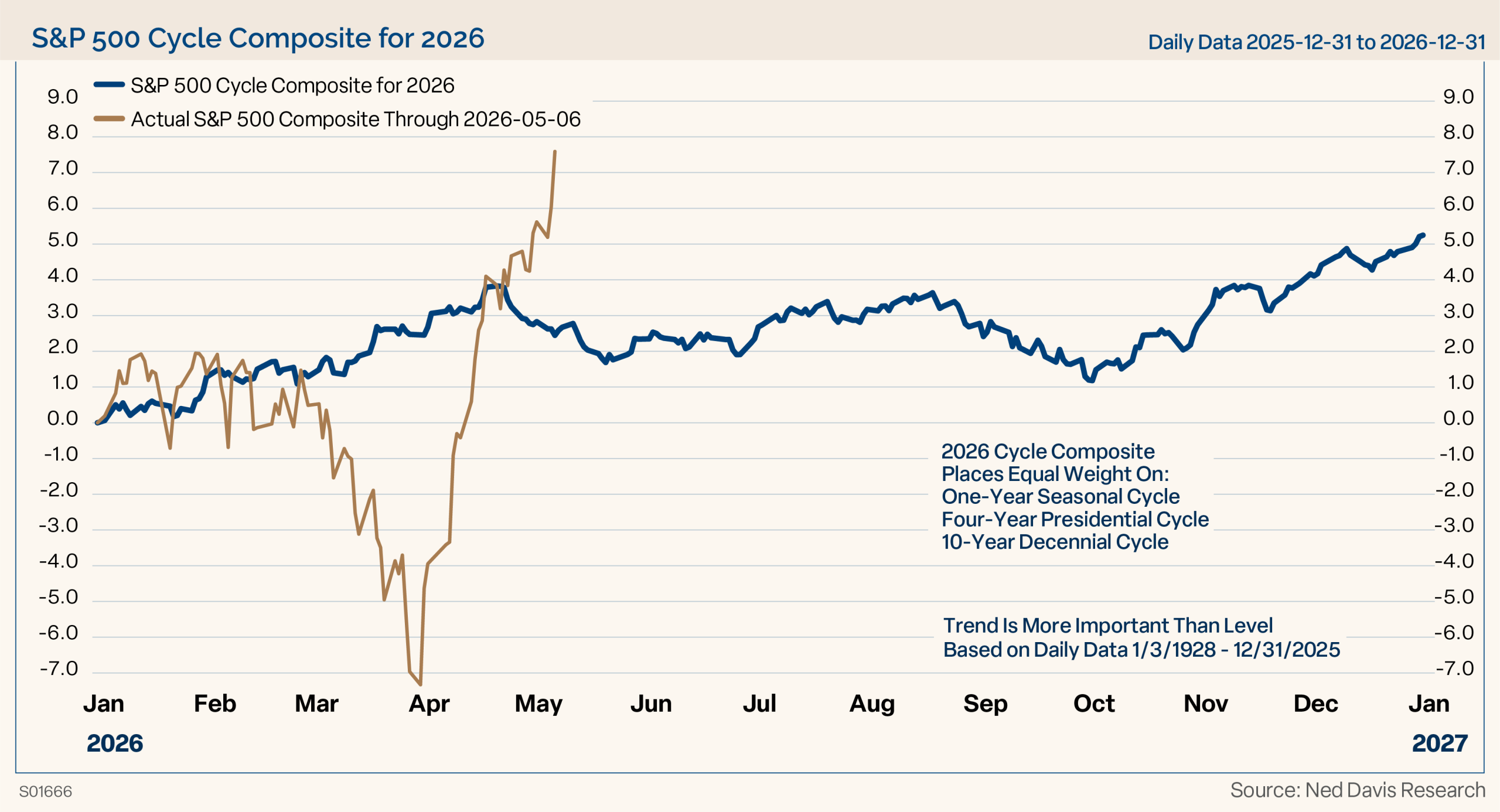

Figure 5 shows the Ned Davis Research Cycle Composite for this year. It combines the one-year cycle, four-year cycle (election years), and decennial cycle into a single composite. The blue line is the composite, and the gold line is the actual S&P 500. We use the Cycle Composite as a guide to how the market may trade directionally in the upcoming year. It has had a very good track record in previous years.

Figure 5

For illustrative purposes only. Past performance is not indicative of future results.

Overall, the composite suggested another good year for stocks but with some middle of the year volatility. In our Annual Outlook, we said, “The first half of 2026 could see a correction if bond yields rise significantly, given mounting concerns that monetary and fiscal policies might be overly stimulative.” We did have a correction in the first quarter, and bond yields rose with the 10-year yield hitting 4.67% in response to geopolitics and inflation pressures from oil and energy costs.

We expect to see some volatility in the second half of the year, but we are also mindful of the fact that the first quarter correction from the Iran conflict may have front loaded some of the normal midterm election year correction. Time will tell.

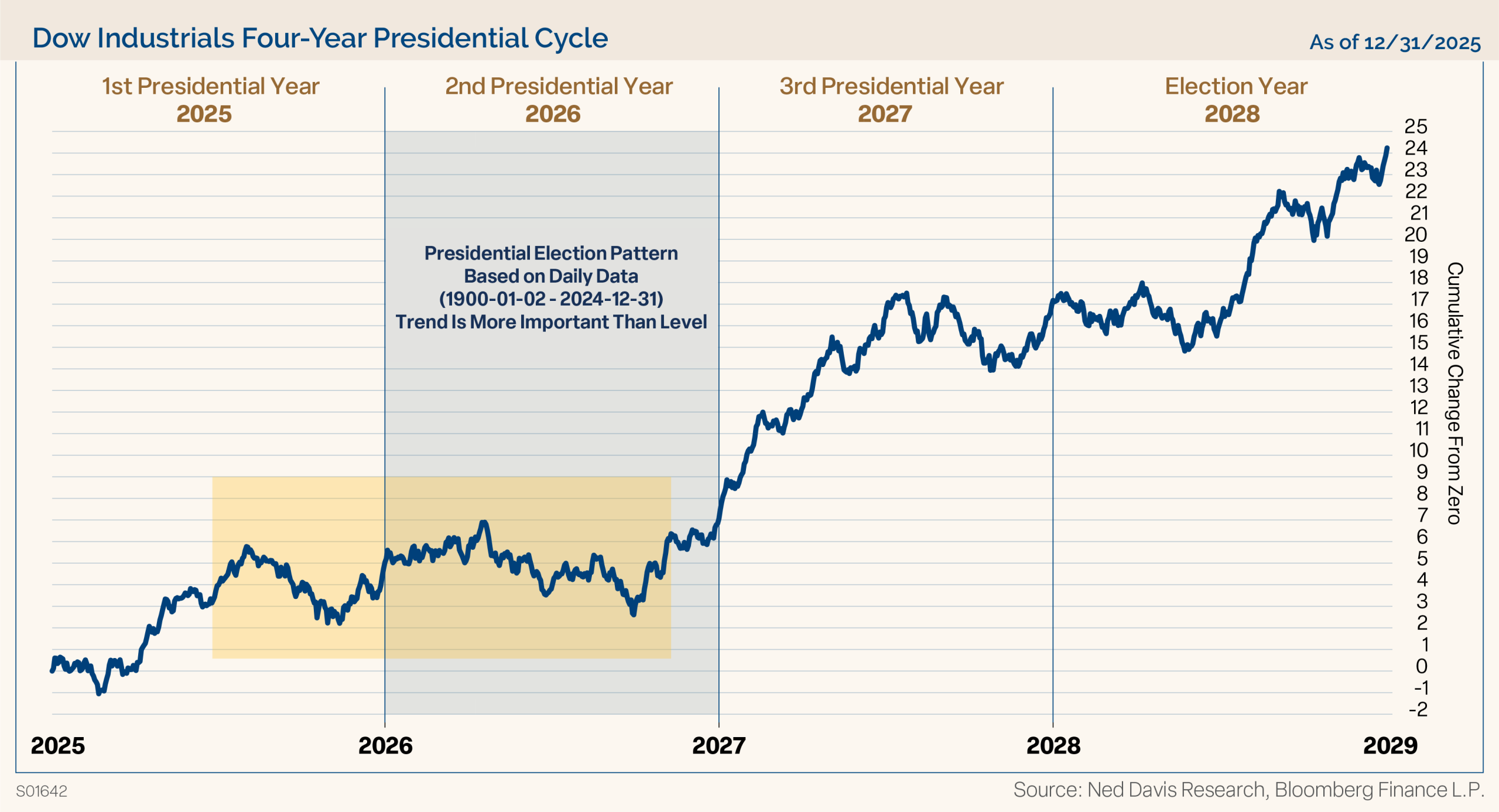

Figure 6 shows the historical trend of the market during the four years of the Presidential Cycle. The horizontal shaded zone from about the middle of the first year of the term into midterm elections shows that historically the market normally trades in a sideways consolidation into the midterm elections.

Figure 6

For illustrative purposes only. Past performance is not indicative of future results.

Overall, the second year of the President’s term has been mediocre for the equity markets. In the post WWII era (since 1948), the S&P 500 has delivered an average gain of just 4.6% in midterm election years, posting positive returns only 58% of the time. This time the market has been much stronger than the historic average, with an earnings-led bull market driving stocks higher. We were much more bullish coming into the year. Our S&P 500 target for year end was 7700, which would have been a 12.5% advance. Strong earnings have led us to raise that target to 8100.

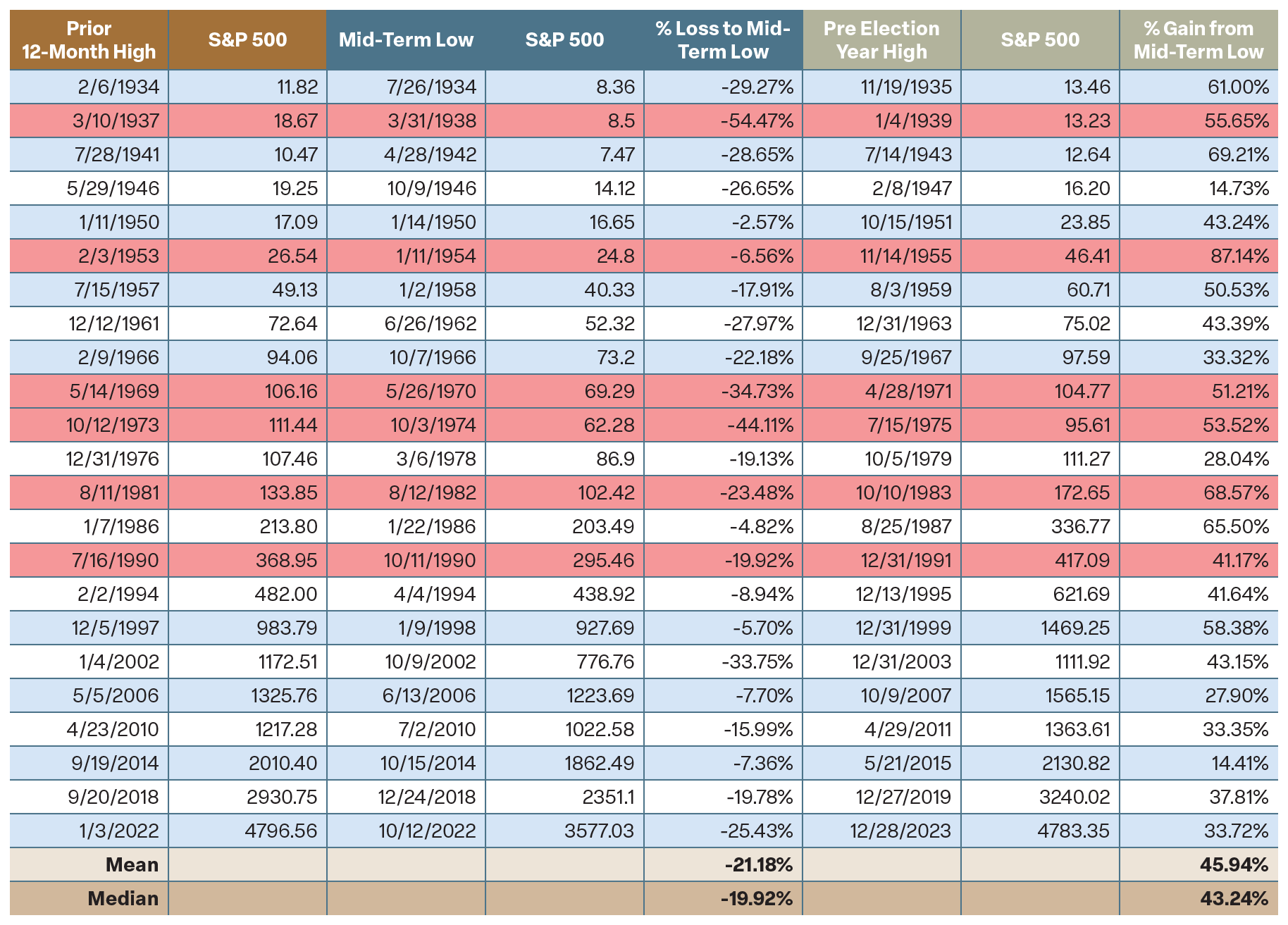

Figure 7 is busy, but it contains a lot of good historical information. In summary, it shows every midterm election year since 1934, the corrections into the midterm market lows, and the rebound rallies following those lows.

Figure 7 – S&P 500 Midterm Year Performance Since 1934

Source: Bloomberg. For illustrative purposes only. Past performance is not indicative of future results.

History shows that the market has endured a 21% correction on average into midterm election year lows. The silver lining is that the market has also historically rebounded very strongly from those midterm lows to a high the very next year. The average gain from the midterm low to the high point in the following year is 46%.

We are mindful of the historic precedent and would use any pullback or correction as a buying opportunity given the sense of pessimism by individual investors, strong fundamentals, and corporate earnings.

Markets are cyclical, and corrections are normal. On average, the S&P 500 has experienced three 5% corrections a year, a 10% decline once a year, a 15% decline every two years, and a 20% or greater bear market every three years.

Last year, the S&P 500 suffered an 18.9% correction in the aftermath of tariff liberation day and rebounded sharply. This year, from peak to low on March 30, the S&P 500 declined by 9%, before again rebounding sharply to new all-time highs.

The market hasn’t had a true 20% decline since 2022, and each calendar year since then, the market has been up double digits.

Pessimism Persists, Which May Be Good News

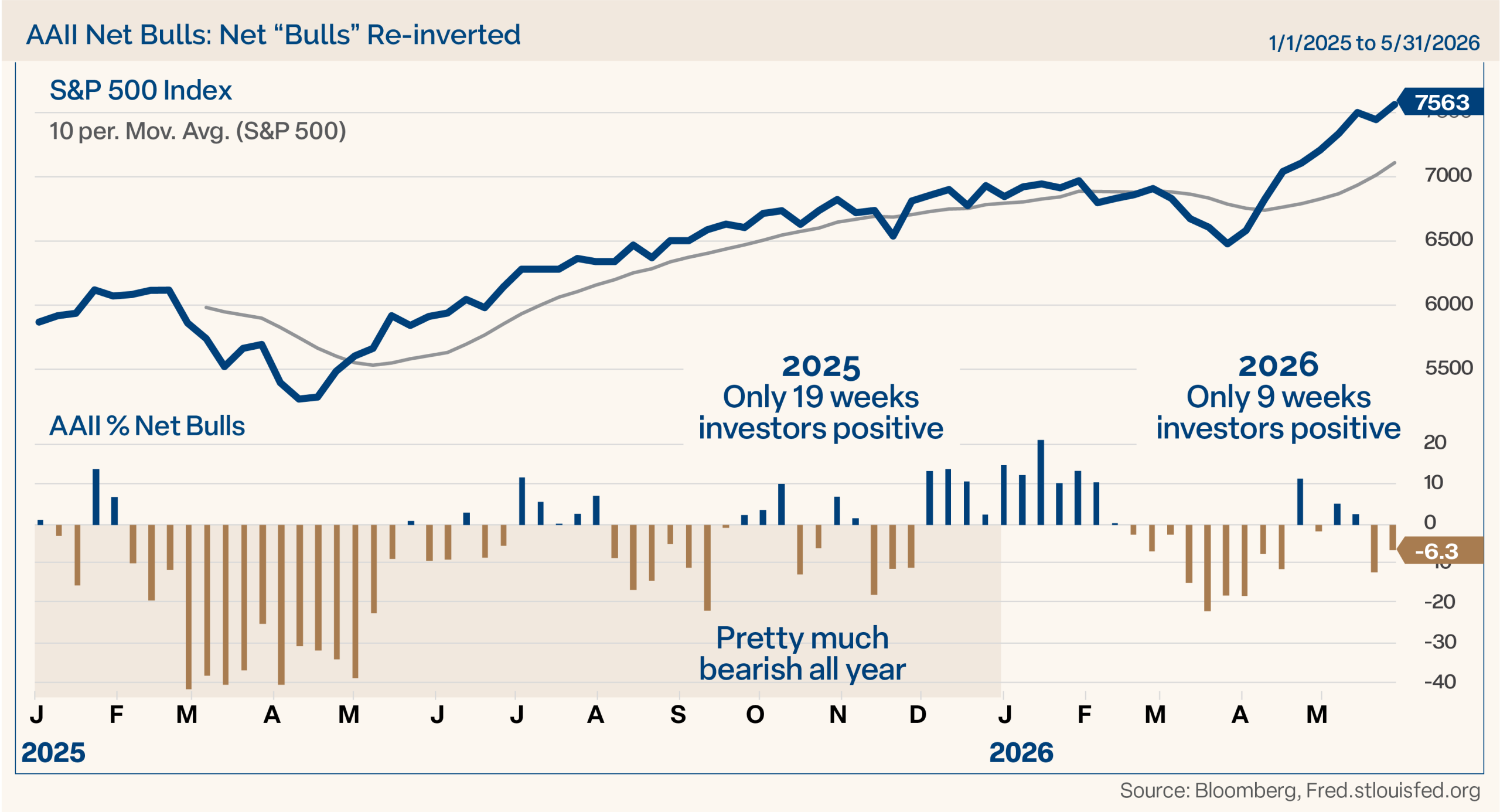

Let’s turn to investor sentiment. For the stock market, fundamentals and earnings matter over the long run. In the short run, however, sentiment matters. We know that markets climb a “wall of worry,” and investors seem to be fretting about a lot of things these days.

The American Association of Individual Investors (AAII) sentiment poll showed a long stretch of excessive pessimism from last year and into this year. (Figure 8.) Investors were more bullish than bearish in only 19 weeks last year, and only nine weeks so far this year.

Figure 8

For illustrative purposes only. Past performance is not indicative of future results.

In early April, 52% of investors were bearish. The only times higher in past 10 years were during COVID, the 2022 Russia invasion of Ukraine, and the period after tariff liberation day.

Currently 47.7% are bearish and only 30.4% are bullish. Those are crazy pessimistic stats given the markets are trading at or near all-time highs after three years in a row of double-digit gains. As Warren Buffett said, “Be fearful when others are greedy, and greedy when others are fearful.” In our opinion, investors are still too pessimistic.

Another sentiment measure is cash on the sidelines. Money doesn’t grow on trees, but apparently assets in money market funds can grow to the sky. ICI data shows that total assets in money market funds have reached a record $7.9 trillion. That is a lot of dry powder to potentially come off the sidelines. We certainly don’t expect it all to flow into the market, but around the margin there is a lot of cash to deploy into the market. The large amount of cash on the sidelines could help keep corrections in check. Liquidity is abundant, and that is a positive factor for the markets.

Ironically, Americans have never been richer and, at the same time, more pessimistic about the economy. The Michigan Consumer Sentiment Index is at a record low. It has been definitely impacted by the war, inflation, gas prices, and other factors. However, the market is at all-time highs, home ownership is at a record 65%, two-thirds of American households own stocks, the unemployment rate is 4.3%, and yet, we are currently sitting at the lowest level of consumer sentiment in the past 75 years. It’s lower than the global financial crisis, the dot-com crash, the Carter-Reagan recession, 1970s inflation, and the start of the COVID pandemic.

The silver lining is that the market historically does very well when consumer sentiment is depressed.

Fundamentals Remain the Foundation of This Rally

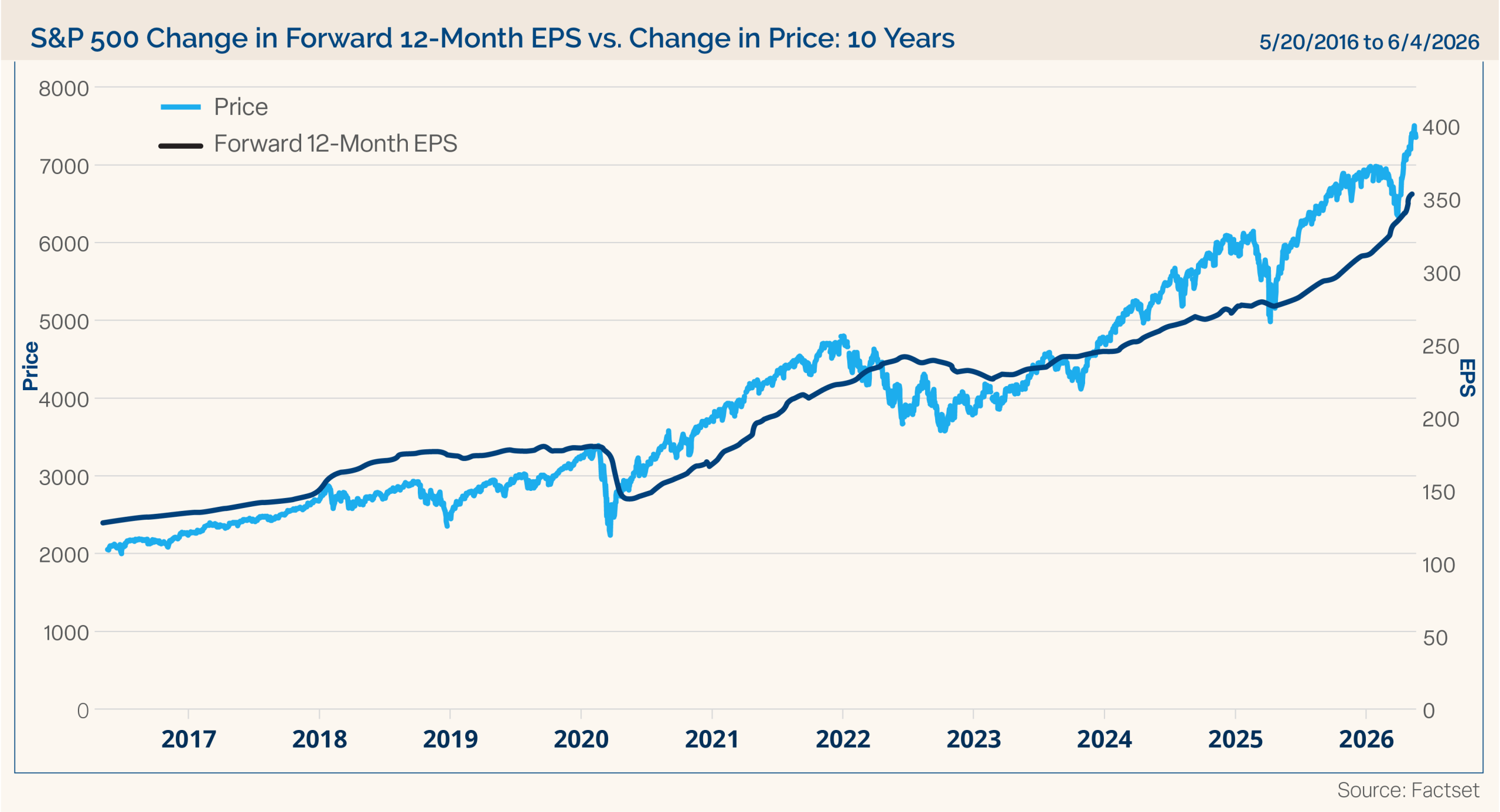

Over time, stock prices and earnings growth are correlated; economic growth generates earnings. Higher earnings have led to higher stock prices, and in times of earnings declines, stocks have followed suit. In Figure 9, we show the S&P 500, realized earnings, and forward expected earnings over the next 12 months.

Figure 9

For illustrative purposes only. Past performance is not indicative of future results.

Actual corporate earnings have surged to new highs, and expected forward earnings are also out to new highs for the S&P 500, mid-cap and small-cap indices. We expected strong corporate earnings to drive stocks higher in an earnings-led bull market.

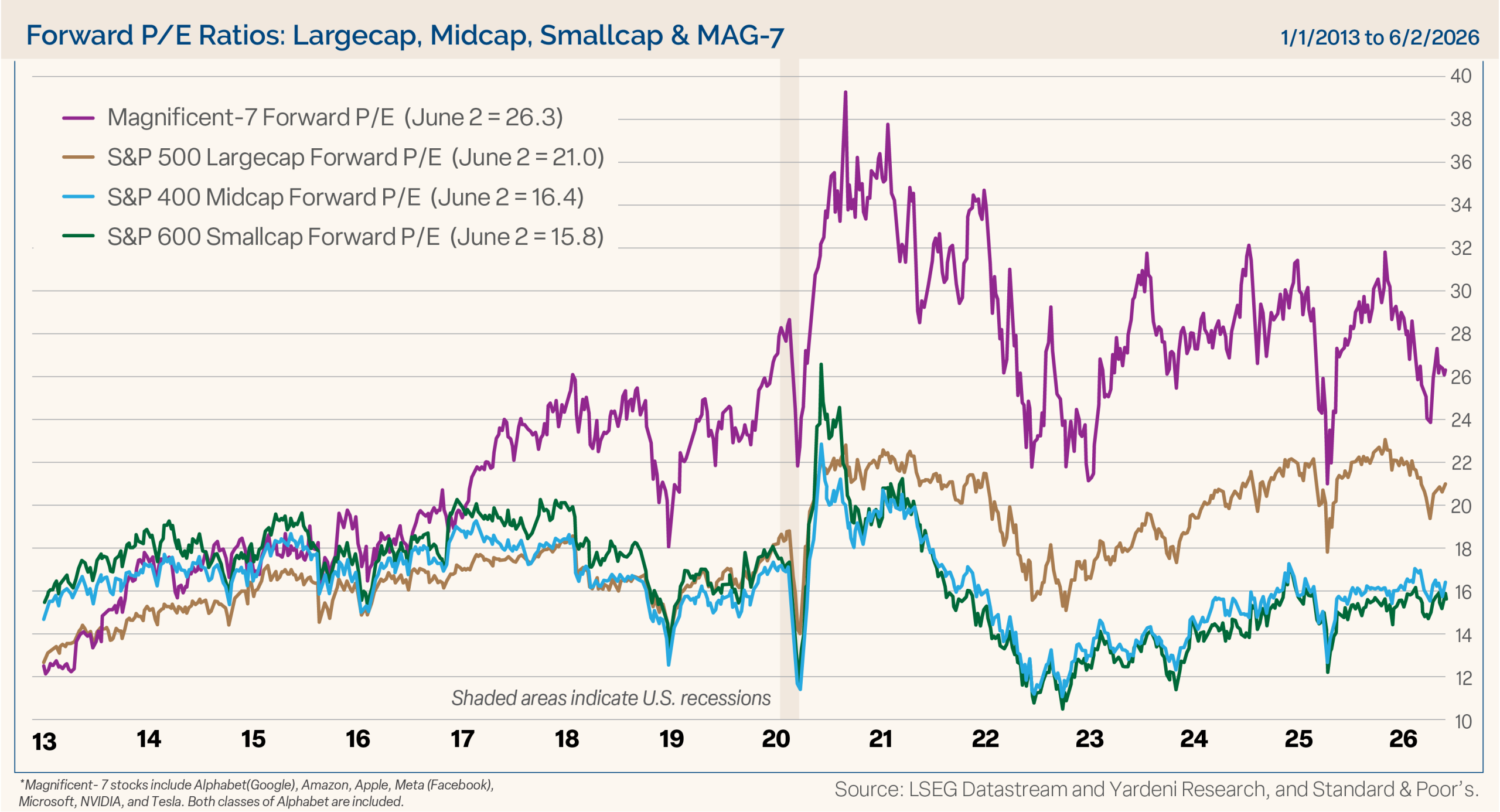

Looking at valuations, as shown in Figure 10, price-to-earnings (P/E) multiples have come down since the beginning of the year. Earnings growth has outpaced stock price advances. Coming into this year, the S&P 500 traded at a forward P/E of 22.1; it now trades at 21 times earnings. The Magnificent 7 forward P/E is 26.3, down from 28.6 to start the year and down from a 38 multiple at its peak. Small- and mid-cap stocks trade at much more reasonable 15 to 16 times forward earnings.

Figure 10

For illustrative purposes only. Past performance is not indicative of future results.

As we said in our Annual Outlook, “We know valuations are a very poor timing tool, as the market can stay rich for extended periods, but they do tell us that risks are elevated if earnings growth doesn’t materialize.” Going forward, we expect earnings growth will continue to drive the market.

Earnings grew by double digits for the sixth consecutive quarter in the first quarter, the longest streak since the earnings recovery following the GFC.

Industry analysts are very optimistic about earnings this year, with expectations of double-digit gains for all four quarters. Analysts continue to raise expectations. From the end of last year to now, analysts have increased their earnings target by 7%. Normally as the year progresses, analysts lower their expectations.

As shown in Figure 11, earnings trends are also broadening out. Tech is the largest contributor by far, but Communication Services, Energy, Financials, Industrials, and others are showing strength. Analysts now expect earnings to grow by 24% this year, followed by 17% in 2027.

Figure 11

For illustrative purposes only. Past performance is not indicative of future results.

At the beginning of the year, applying a 22x forward multiple to expected 2027 earnings yielded a year-end S&P 500 target of 7700. Now, a forward P/E of 21 and expected earnings per share of $385 in 2027 implies an upside near 8100.

A big reason earnings growth needs to drive the market is that in real terms, the S&P 500 is extended way above its longer-term trendline. In fact, it’s the highest overbought condition since 1929. Of course, overbought conditions can stay that way for long periods. It does suggest that risks are present.

Another measure that urges caution over the long term, and for investors to prepare for lower returns, is a version of Warren Buffet’s favorite valuation indicator that compares the stock market capitalization to the size of the economy. It currently shows that stocks have run ahead of the economy. Of course, the economy is undergoing massive structural changes with AI, productivity growth, and energy independence. I would be less worried about the long-term outlook if the economy can increase its growth rate and corporate earnings continue to thrive.

The Fed Is Between a Rock and a Hard Place

Turning to the Fed, they are under a microscope, and between a rock and a hard place. Art Cashin, a floor trader on the NYSE, was a fixture on CNBC and was known for saying, “Bull markets don’t die of old age, they’re killed by the Fed.” We don’t believe the Fed is ready to kill the bull. Let’s take a look.

June 17 concluded the first Federal Open Market Committee (FOMC) meeting with Kevin Warsh at the helm. Warsh knows President Trump wants the Fed to cut rates, but economic data makes that highly unlikely. A unique set of circumstances around this Fed is that former Fed Chair Powell still has a seat at the table.

As expected, the Fed left rates unchanged but shifted to a more hawkish bias, upgrading their assessment of overall inflation to 3.6% and core inflation to 3.3%, and downgraded their GDP forecast to 2.2%. Half of the Fed officials now expect at least one rate hike this year.

The market historically challenges new Fed chairs with an average maximum drawdown of 14.8% in the first six months of the new term. The last three drawdowns were milder: Bernanke (-8.0%), Yellen (-3.8%), and Powell (-8.5%). This is one of many factors that could cause a market correction in the second half of the year. The depth of a drawdown likely depends on any real or perceived challenges to the Fed’s independence and changes to policy or future communications from the Federal Reserve.

The Fed chair often gets the attention, but the Fed is not a one person show. While the Fed chair is the most visible, there are 12 votes that count! It is a committee; new Fed Chair Warsh and former Fed Chair Powell (still on the Fed) each get one vote.

Warsh has repeatedly signaled a preference for both lower policy rates and a smaller Fed balance sheet. Achieving both will be difficult in a world of large fiscal deficits and heavy Treasury issuance.

Moving forward, we think the shape of the yield curve will be just as important if not more than the level of overnight rates. The bond vigilantes will be out in force if they disagree with the Fed’s policy path.

Energy Prices Reignite Inflation but Relief May Be on the Way

We had a benign outlook on inflation coming into the year, expecting it to gradually decline as housing costs exerted downward pressure on headline inflation. On the positive side, tariff policy has eased with the anniversary of tariffs, and the Supreme Court ruling to terminate International Emergency Economic Powers Act (IEEPA) tariffs in the first quarter. While still above the Fed’s target, inflation had been cooling until it did an about face at the same time the conflict in Iran began. It’s all about oil and energy costs. The war in Iran, now in its fourth month, drove up oil and other commodity prices and caused supply chain snarls.

The latest inflation readings have PPI at 6.5%, CPI at 4.2%, and the Fed’s preferred measure Core PCE, a more muted 3.3% year over year. The Fed’s attention is squarely on inflation, and now less dovish, even with Warsh at the helm.

We’re seeing some relief in gasoline and oil prices from their recent peaks. The daily national average of gasoline prices in down 12% and West Texas Intermediate (WTI) is off its peak of $113 to $76/barrel, down 33% off its peak and up just 17% from pre-Iran conflict levels. Declining oil prices should filter through to inflation expectations and reduce the Fed’s need to hike rates.

Credit leads and total return indices are at new highs. There is no stress in public credit markets, and abundant liquidity provides a supportive backdrop. Across the credit spectrum, spreads are near record lows. For example, high yield spreads are currently 261 basis points (bps). In January, they hit 250 bps, the lowest spread for the high yield index since June 2007, before the start of the GFC. With spreads this low, we don’t expect to see much more compression, therefore, returns moving forward will likely be more from coupon.

The market continues to wrestle with the same tension that has defined recent months, historically rich spread valuations alongside still attractive all-in yields. Absolute yields remain supportive of demand. Every time we see yields move a touch higher, more buying demand comes into the market. In our opinion, it is a yield-driven market until further notice.

The Fed is caught between labor market dynamics and inflation. What was a no hire/no fire labor market over the past year is now gradually improving but not overheating. The Fed feels pressure from inflation due to rising energy prices. However, Fed policy is powerless to influence supply shocks like we have now.

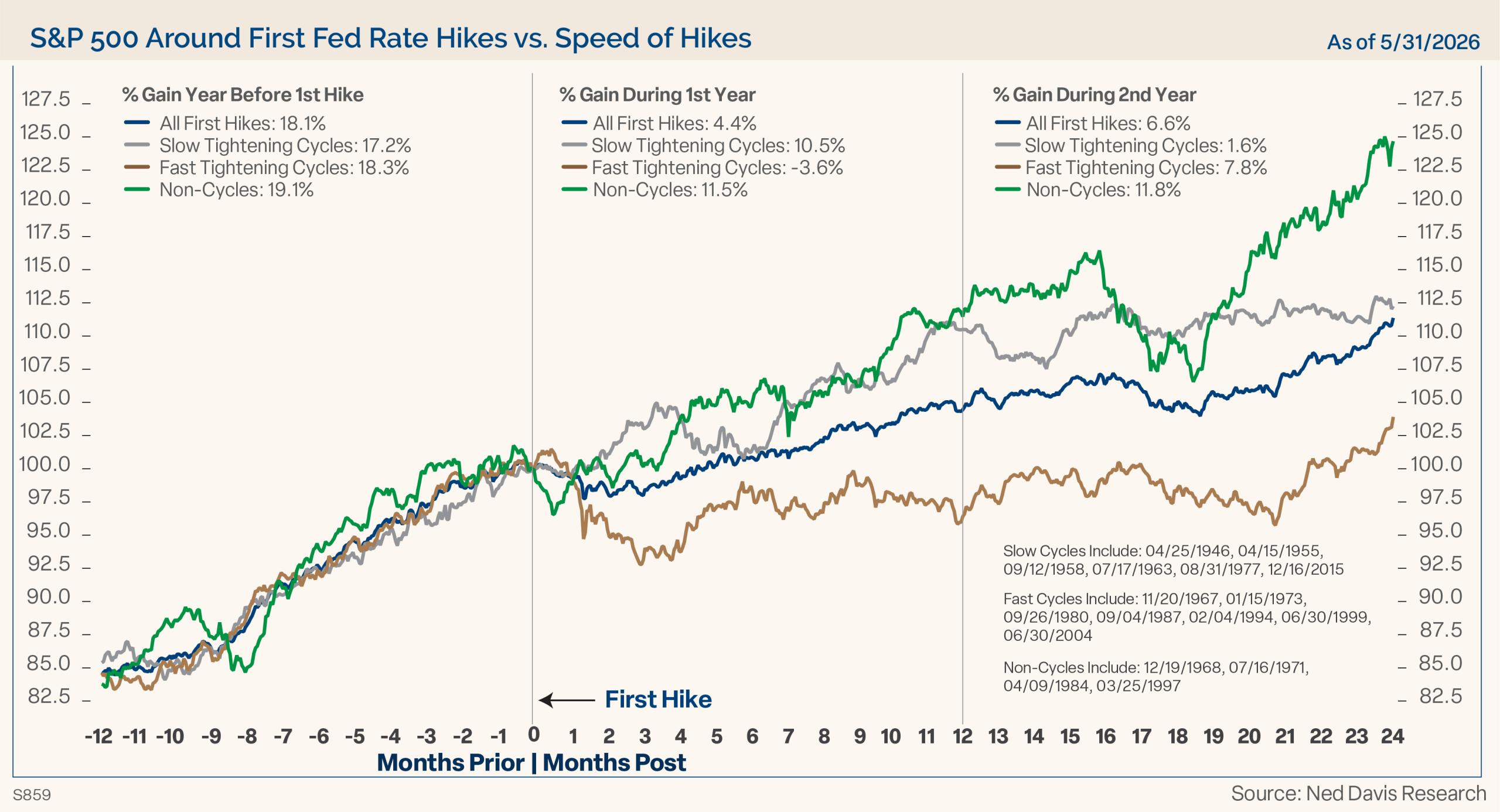

While we think the Fed is in a protracted holding pattern on rates, the market has priced out rate cuts, and the market expects the Fed’s next move to be a rate hike, potentially near year end or early next year. If the Fed does hike, we think it would be a slow cycle, more of an insurance hike against inflation. Figure 12 shows the difference between rate hike cycles. For example, in a slow hike cycle, the S&P 500 has gained an average of 10.5% in the first year following the hike, while in fast cycles it has lost 3.6% one year later.

Figure 12

For illustrative purposes only. Past performance is not indicative of future results.

Of course, as we expect, there is a chance that the Fed does nothing for the remainder of the year.

Geopolitical Shocks Sting Less Than They Used To

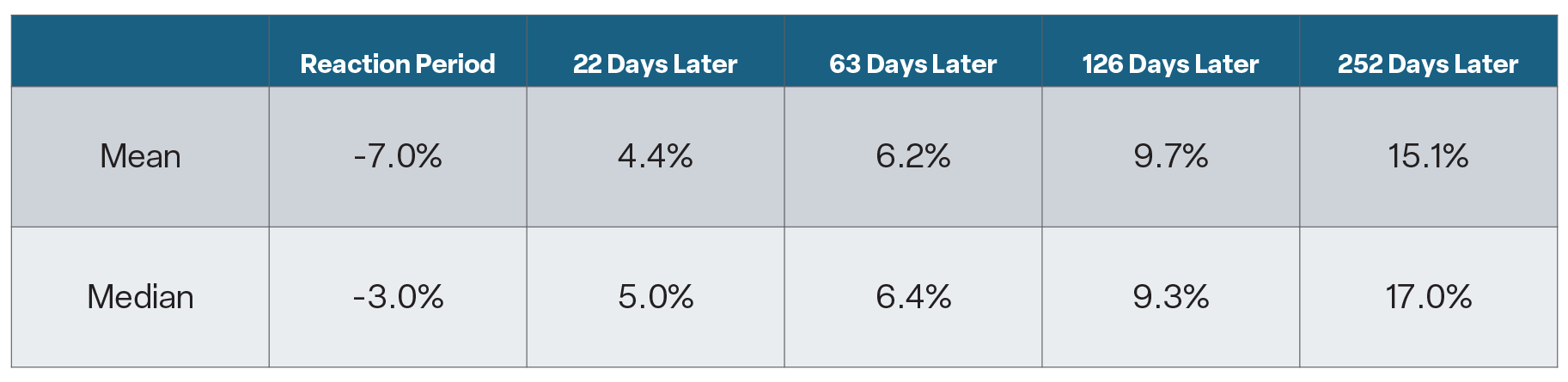

Finally, let’s look at crisis events and the state of the oil market. Figure 13 shows the market impact from 59 crisis events dating back to 1907.

Figure 13 – Crisis Events and Subsequent DJIA Performance

For illustrative purposes only. Past performance is not indicative of future results

Notes: 59 crisis events since 1907. Data Price Only.

Source: S&P Dow Jones Indices

The average decline during the initial knee jerk reaction was 7% as investors typically sell first and assess later. One, three, six, and 12 months after the initial drawdown are all positive and, in fact, better than normal average gains.

The crisis script played out pretty much as expected this time. The S&P 500 fell by 7.7% during the initial reaction, then rallied 13.7% one month after bottoming. It is up 19.4% since the March 30 lows.

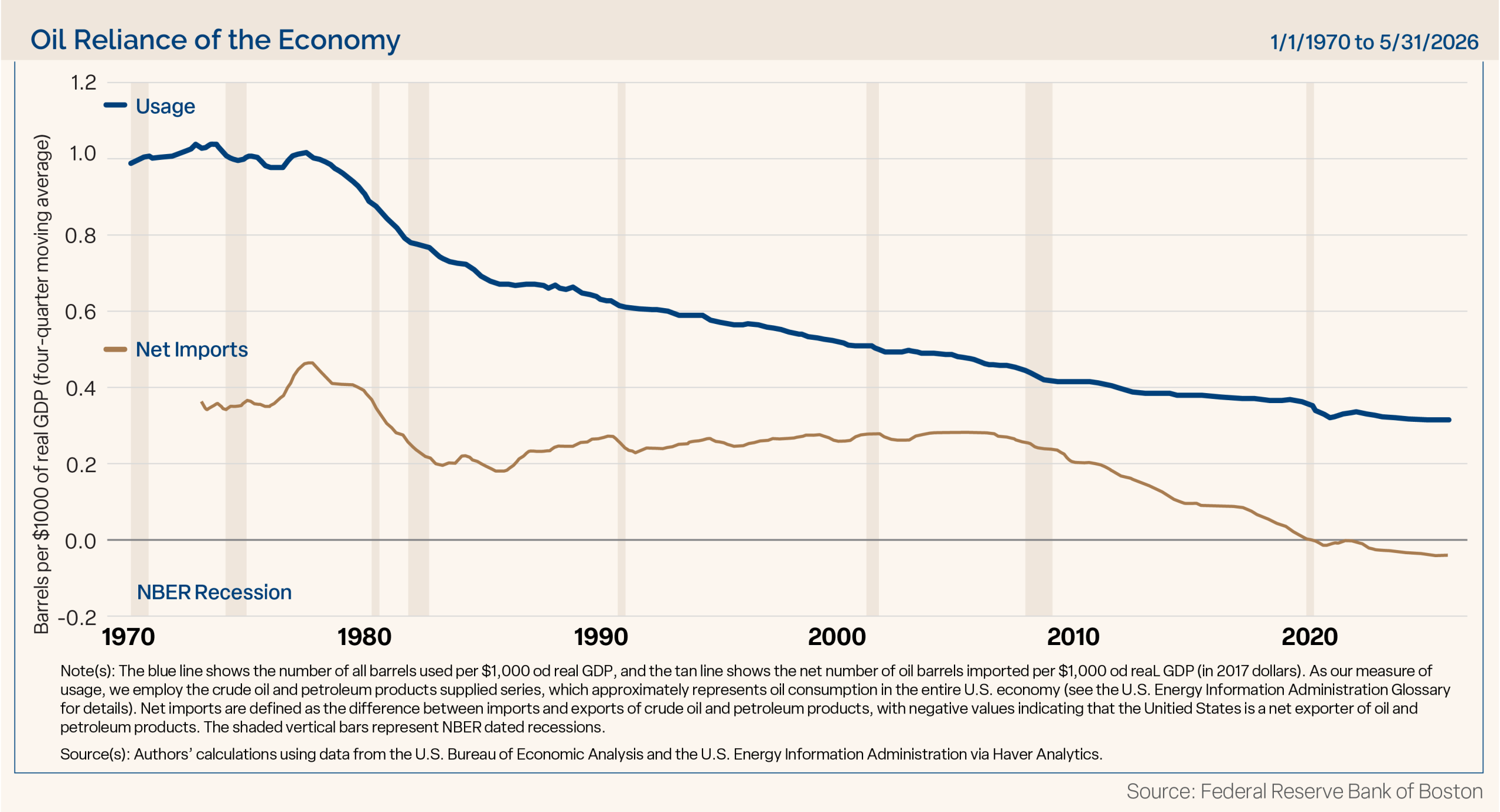

Earlier this month, the Federal Reserve Bank of Boston published a paper titled “Reassessing the US Economy’s Vulnerability to Oil Shocks.” (See Figure 14.)

Figure 14

For illustrative purposes only. Past performance is not indicative of future results.

forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

Several conclusions of the paper are:

- The U.S. economy has become far less dependent on oil over time. Today, the U.S. economy’s oil reliance is less than one-third of what it was in the 1970s, reflecting greater efficiency in oil use and a structural shift away from energy-intensive goods manufacturing and toward services.

- While the country’s oil usage has also declined, domestic oil production has grown, substantially reducing reliance on foreign oil supplies. Net oil import reliance began falling rapidly around 2010 due to the shale oil boom, and by 2019, the U.S. became a net oil exporter.

- The decline in oil reliance suggests that oil is now less central to the U.S. economy than ever before, and shocks are less likely to have the same magnitude.

As noted in the minutes of the April FOMC meeting, structural changes to the U.S. economy could cushion the impact of the shock.

Oil shocks today are associated with less of an impact on PCE inflation relative to the impact of comparable shocks four or five decades ago. For example, a 33% real oil price shock, an estimate of the shock this time, is now associated with a 1.5% increase in PCE inflation over the next year, about

1/3 less than in the mid-1970s.

The longer oil remains elevated the more inflation will linger. Currently, WTI is up 17% from pre-Iran conflict, at about $76 / barrel down from an early April high of $113/barrel.

Looking Ahead, Staying the Course

Markets rarely move in a straight line, and this year has been no exception. But through geopolitical shocks, a change in Fed leadership, and persistent investor pessimism, the fundamental case for equities remains intact. Corporate earnings continue to set records, the economy is growing, and history suggests that corrections in midterm election years give way to some of the strongest rallies in the market cycle.

We remain vigilant about the risks ahead — a new Fed chair, elevated valuations, and lingering inflation — but the weight of the evidence continues to favor equities. Advisors who keep their clients focused on fundamentals and help them resist the pull of pessimism are, in our view, best positioned to deliver value in the months ahead.

The opinions expressed are those of Clark Capital Management Group. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Clark Capital investment portfolio. Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies. For educational use only. This information is not intended to serve as investment advice. This material is not intended to be relied upon as a forecast or research. Investors must make their own decisions based on their specific investment objectives and financial circumstances. Past performance does not guarantee future results.

This document may contain certain information that constitutes forward-looking statements which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology (or the negative thereof). No assurance, representation, or warranty is made by any person that any of Clark Capital’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

Clark Capital Management Group, Inc. is an investment adviser registered with the U.S. Securities and Exchange. Commission Registration does not imply a certain level of skill or training. More information about Clark Capital’s advisory services can be found in its Form ADV and/or CRS, which are which is available upon request.

The Barclays U.S. Corporate High-Yield Index covers the USD-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P

is Ba1/BB+/BB+ or below.

Fixed income securities are subject to certain risks including, but not limited to: interest rate (changes in interest rates may cause a decline in market value or an investment), credit, prepayment, call (some bonds allow the issuer to call a bond for redemption before it matures), and extension (principal repayments may not occur as quickly as anticipated, causing the expected maturity of a security to increase).

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater

market fluctuations, risk of default or loss of income and principal than higher-rated securities.

The S&P 500 measures the performance of the 500 leading companies in leading industries of the U.S. economy, capturing 75% of U.S. equities.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values.

The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 1000 Index measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 1000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000 represents approximately 92% of the U.S. market.

The Russell 2000 Index measures the performance of the 2000 smallest U.S. companies based on total market capitalization in the Russell 3000, which represents approximately 10% of Russell 3000 total market capitalization.

The Russell 3000 Index measures the performance of the 3000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

The MSCI USA Index is designed to measure the performance of the large and mid cap

segments of the US market.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

The MSCI World ex US Index is a market capitalization-weighted index designed to measure equity performance in 22 global developed markets, excluding the United States. The benchmark for this composite is used because the MSCI World Ex US Net Index is generally representative of international equities.

BBgBarc U.S. Aggregate Bond Index covers the U.S. investment-grade fixed-rate bond market, including government and credit securities, agency mortgage pass-through securities, asset-backed securities and commercial mortgage-based securities. To qualify for inclusion, a bond or security must have at least one year to final maturity, and be rated investment grade Baa3 or better, dollar denominated, non-convertible, fixed rate and publicly issued.

The BBgBarc US Treasury Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint but are part of a separate Short Treasury Index. STRIPS are excluded from the index because their inclusion would result in double-counting. The US Treasury Index is a component of the US Aggregate, US Universal, Global Aggregate and Global Treasury Indices.

The BBgBarc US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility and financial issuers. The US Corporate Index is a component of the US Credit and US Aggregate Indices, and provided the necessary inclusion rules are met, US Corporate Index securities also contribute to the multi-currency Global Aggregate Index.

The BBgBarc U.S. Municipal Index covers the USD-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds.

Created by the Chicago Board Options Exchange (CBOE), the Volatility Index, or VIX, is a real-time market index that represents the market’s expectation of 30-day forward-looking volatility. Derived from the price inputs of the S&P 500 index options, it provides a measure of market risk and investors’ sentiments.

The Institute of Supply Management (ISM) Non-Manufacturing Index is an economic index based on surveys of more than 400 non-manufacturing (or services) firms’ purchasing and supply executives.

Gross domestic product (GDP) is the standard measure of the value added created through the production of goods and services in a country during a certain period.

GDPNow is not an official forecast of the Atlanta Fed. Rather, it is best viewed as a running estimate of real GDP growth based on available economic data for the current measured quarter.

The 10 year treasury yield indicates the interest rate that the US government pays to borrow money for a 10-year period.

References to market or composite indices or other measures of relative market performance over a specified period of time are provided for your information only. Reference to an index does not imply that your account will achieve returns, volatility or other results similar to that index. The composition of the index may not reflect the manner in which a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, restrictions, sectors, correlations, concentrations, volatility or tracking error targets, all of which are subject to change. Investors cannot invest directly in indices.

A leading indicator is a measurable set of data that may help to forecast future economic activity. Leading economic indicators can be used to predict changes in the economy before the economy begins to shift in a particular direction.

The Consumer Price Index (CPI) measures the change in prices paid by consumers for goods and services. The CPI reflects spending patterns for each of two population groups: all urban consumers and urban wage earners and clerical workers.

Core inflation removes the CPI components that can exhibit large amounts of volatility from month to month.

The Producer Price Index (PPI) measures the average change over time in the prices domestic producers receive for their output.

The ISM Prices Paid represents business sentiment regarding future inflation. A high reading is seen as positive for the USD, while a low reading is seen as negative.

Nonfarm payroll refers to the number of jobs in the private sector and government agencies. It excludes farm workers, private household employees, proprietors, non-profit employees, and actively serving military.

Core PCE, or Core Personal Consumption Expenditures, is a measure of inflation that excludes food and energy prices. It represents the prices of goods and services purchased by consumers, but with the most volatile components (food and energy) removed to provide a clearer picture of underlying inflation trends. The Federal Reserve uses Core PCE as a key indicator when making monetary policy decisions.

VIX of VIX (or VVIX) is a measure of the volatility of the Chicago Board Options Exchange (CBOE) Volatility Index (VIX). The CBOE’s VIX measures the short-term volatility of the S&P 500 indexes, and the VVIX measures the volatility of the price of the VIX. In other words, VVIX is a measure of the volatility of the S&P 500 index and alludes to how quickly market sentiment changes.