The market has reacted very negatively to macroeconomic data, which showed that the pace of economic activity has slowed in recent months. The market began selling off sharply at the end of last week and the selling pressure continued on Monday. The market is pricing in a policy mistake by the Fed with new recession fears and is worried that the Fed is now behind the curve. We believe that is probably an overreaction.

Friday’s employment report highlighted that labor market conditions have softened. The economy still created 114,000 jobs in July, but it was well short of the 175,000 expected, and the unemployment rate rose to 4.3%. In our Mid-Year Market Outlook in June, we highlighted the rise in the unemployment rate, which at the time, was 4.0%. It is now 4.3% and higher than the Fed’s own year-end target in their Summary of Economic Projections. In the Outlook we said, “Count us among those that think the Fed should act soon to recalibrate monetary policy.” The market is now on board with that sentiment, too.

At the beginning of the year, we were calling for four Fed rate cuts to recalibrate policy given that inflation peaked and was declining sharply. By keeping rates elevated, the Fed was by default tightening policy as inflation moderated. The market expectations of rate cuts have been all over the place this year, from 6.5 cuts to 1 cut. Now, the market is pricing in the equivalent of 4.5 rate cuts by year end, with the first cut likely to be 0.50% at the September 18th FOMC meeting or sooner.

It’s important to remember that markets are cyclical, and corrections are normal. On average, the S&P 500 has experienced three 5% corrections a year, a 10% decline once a year, a 15% decline every two years, and a 20% or greater bear market every three years. The major indices have behaved in a cyclical manner since the bear market lows in October 2022. There have now been four 5% or greater corrections in the S&P 500 and one 10% correction. From its recent peak on 7/16, the S&P 500 has declined 8.5%. Small-cap stocks and large-cap growth have corrected more than the broad S&P 500. The Russell 2000 has declined 9.9% and the Russell 1000 Growth is off over 13.1%.

The wall of worry is mounting. Global equity markets gapped lower to begin trading on Monday morning. The CBOE Volatility Index (VIX) surged, the Japanese Nikkei Index had its largest three-day drop in its history (-19.55%), and the NASDAQ is in correction territory. Meanwhile, our credit models remain in a risk-on position. The Bloomberg US Corporate High Yield Bond Index ended July trading at a new all-time high and investment grade corporate debt also surged higher as duration benefited from anticipated rate cuts coming soon.

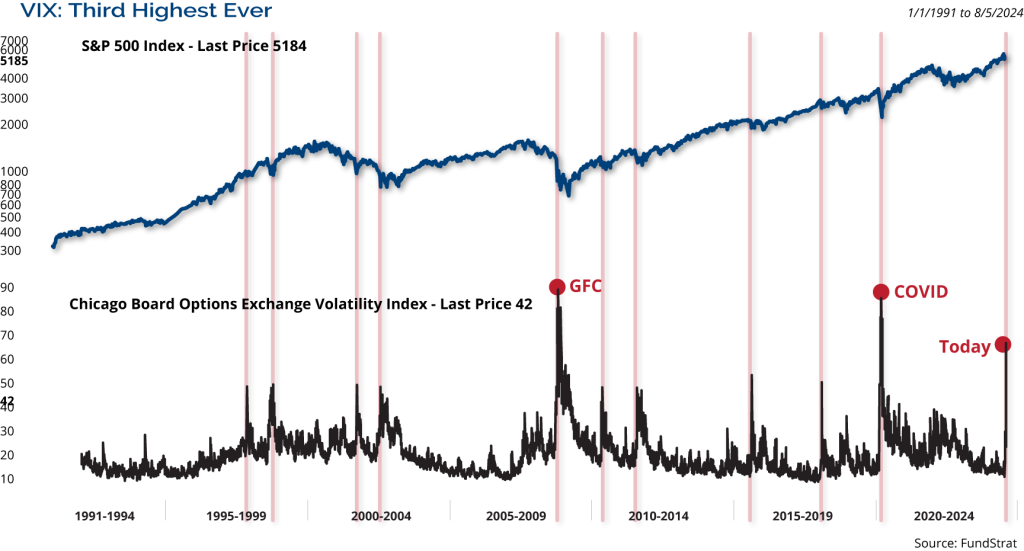

Sentiment statistics have turned from relatively benign to full on panic, seemingly overnight. For example, the VIX Index surged intraday on Monday to its third highest level on record. As shown in the chart below, the only higher VIX levels occurred in 2008 during the Global Financial Crisis and early 2020 in the midst of the COVID market meltdown.

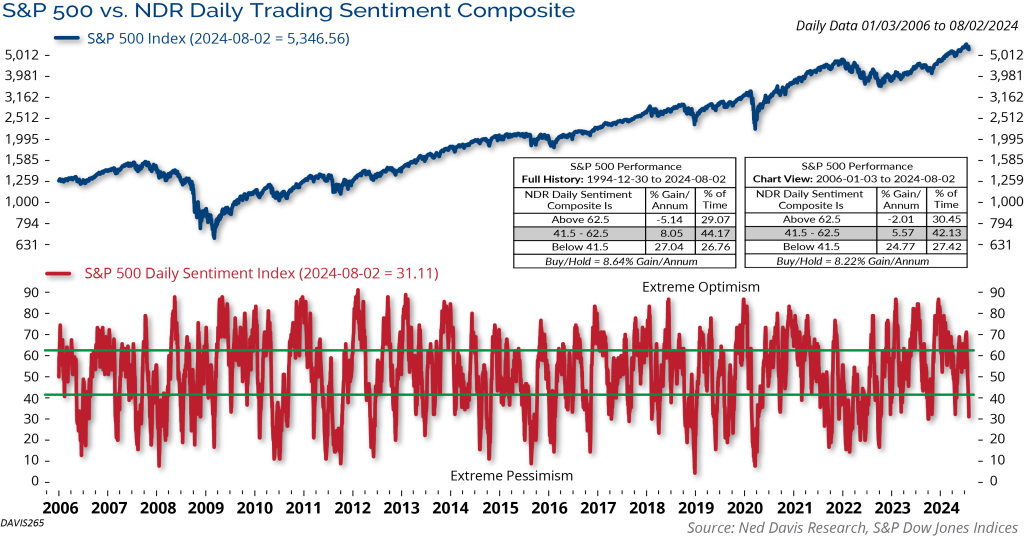

In addition, the Ned Davis Research Daily Trading Sentiment Composite (shown below) dropped into the extreme pessimism zone and should show even deeper levels of extreme pessimism when updated tonight.

The Ned Davis Research Cycle Composite below illustrates the likelihood of election year volatility from August into October. A fair amount of technical damage has been done to the markets during the recent selloff. That will take time to heal once the initial selling pressure exhausts itself. According to FundStrat, since 1950, when the S&P 500 is up more than 10% in the first half of the year (23 instances), August is up only 39% of the time with a median loss of -0.6%. Those have usually been corrections in longer-term uptrends. In those same 23 instances, the S&P 500 experienced a median second half gain of 9.8% with an 83%-win ratio. History suggests this is likely to be a buy the dip event.

However, there is a positive side of the ledger. The broadening of market participation prior to the recent slump, new highs in the NYSE Cumulative Advance-Decline line, and stability in the credit markets all offer a supportive backdrop for risk assets.

Overall, we believe the correction we are in the midst of should be viewed as an overreaction to slowing economic data. The Fed may well be late to begin cutting, but we believe we are experiencing the economic slowdown we have been expecting, and not an economy that is falling off a cliff. Labor markets, while slowing, are still fairly healthy. Importantly, corporate earnings remain solid and should limit additional downside in the equity markets. Meanwhile, bonds have benefited from the increased likelihood of more/sooner Fed rate cuts and have rallied sharply.

We do not believe the pullback is the beginning of a bear market, but rather a correction in an ongoing bull market. As always, we believe it is imperative for investors to stay focused on their long-term goals and not let short-term swings in the market derail them from their longer-term objectives.

This document may contain certain information that constitutes forward-looking statements which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology (or the negative thereof). Forward looking statements cannot be guaranteed. No assurance, representation, or warranty is made by any person that any of Clark Capital’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

The S&P 500 is a stock market index tracking the performance of 500 large companies listed on stock exchanges in the United States.

The CBOE Volatility Index, or VIX, is a real-time market index representing the market’s expectations for volatility over the coming 30 days.

The Japanese Nikkei Index is a stock market index for the Tokyo Stock Exchange. It is a price-weighted index, operating in the Japanese Yen, and its components are reviewed twice a year.

The Bloomberg Barclays U.S. Corporate High-Yield Index covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

Clark Capital Management Group, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital’s advisory services and fees can be found in its Form ADV which is available upon request.