Clark Capital’s Bottom-Up, Fundamental Strategies

Robust corporate earnings, continued AI enthusiasm, and a resilient U.S. economy drove strong markets in May. Technology, semiconductors, and other AI-linked companies remained market leaders, though participation broadened across sectors as confidence in economic growth and profit trends improved.

Macro continues to linger in the background—important, unresolved, and largely ignored until further notice. Treasury yields drifted higher at the front end, while the Strait of Hormuz—a multi-commodity industrial artery—continued to constrain capital goods inputs and contribute to firmer inflation readings (Core PCE and Core CPI), even as oil prices retraced sharply (West Texas Intermediate -17% on the month). Markets also appear to be entering the customary “testing phase” for new Fed leadership, and Kevin Warsh is unlikely to be an exception as his dual mandates of contained inflation and full employment remain in tension.

At the strategy level, we continue to focus efforts in our equity portfolios to own companies we believe are undervalued, high-quality, and demonstrating improving business momentum. In addition, the High Dividend Equity strategy continues a balanced approach prioritizing dividend growth while also seeking exposure to the secular AI buildout.

Below are strategy updates from May:

Navigator® All Cap Core U.S. Equity

- The portfolio is fully invested with ~61.7% in large-cap stocks and the remainder in mid-/small-cap companies and cash.

- The portfolio continues to balance portfolio holdings between established large-cap growth companies and those anti-fragile large-, small-, and mid-cap companies that continue to see strong business momentum.

- The three largest portfolio sectors at the end of the period were Information Technology, Financials, and Communication Services.

- Our current weighting in the Big Six free cash flow margin monopolies is 32.0% vs. approximately 28.8% in the Russell 3000. Information Technology remains the largest sector weight in the strategy at 31.9%, underweight vs. the Russell 3000 benchmark.

- The most recent addition to the portfolio was a U.S. medical device company.

- The two most recent exits were a U.S. medical device company and a major U.S. pharmaceutical distribution company.

Navigator® High Dividend Equity

- The portfolio is positioned with approximately 98.3% in developed countries with the remainder in cash.

- The United States is the largest country weight at 92.8%, followed by the United Kingdom at 3.3%, Switzerland at 1.4%, and Germany at 0.9%.

- Approximately 81.2% of the portfolio is in large-cap stocks with the remainder in mid-/small-cap companies and cash.

- Financials represent the largest sector weight of 18.1%, below the benchmark weight. The next two largest weights are Information Technology and Industrials at 17.9% and 13.4%, respectively.

- Recent additions to the portfolio include a major U.S. technology company and a key supplier of AI server infrastructure as server demand continues to increase, a U.S. data storage company as AI infrastructure drives massive demand for high-capacity storage, and a U.S. biotech company with consistent earnings and a strong drug pipeline.

- The most recent exits were a large U.S. healthcare distribution company and a U.S. biopharmaceutical company.

Navigator® Large Cap Growth

- The portfolio is fully invested with ~86.0% of the portfolio in large-cap stocks and the balance in mid-cap stocks and cash.

- Approximately 99% of total holdings are in developed countries with approximately 94% based in the United States.

- Over 70% of portfolio holdings are derived from the 100 largest cash flow producing companies with high and growing cash flows, high cash flow margins, and increasing sales.

- The three largest portfolio sectors at the end of the period were Information Technology, Communication Services, and Industrials.

- Our current weighting in the Big Six free cash flow margin monopolies is 51.6% vs. approximately 49.8% in the Russell 1000 Growth. Albeit underweight to the benchmark, Information Technology remains the largest sector weight in the strategy at 48.8%.

- The most recent addition to the portfolio was a major Japanese industrial conglomerate.

- The two most recent exits were a U.S. energy technology company and a U.S. medical device company.

Navigator® International Equity ADR

- The portfolio is positioned with ~18.8% in emerging/frontier markets with the balance in developed economies and cash.

- United Kingdom, Japan, Canada, and Spain are the strategy’s largest country weights, all ranging between 7% and 16%.

- The three largest portfolio sectors at the end of the period were Financials, Information Technology, and Industrials.

- The three most recent additions to the portfolio were a cruise and river cruise company, a Swiss-American medical device company, and a South Korean ETF.

- The three most recent exits were the UK’s largest supermarket chain, a Bermuda-based specialty insurer, and a Swiss multinational pharmaceutical company.

Navigator® Small Cap Core U.S. Equity

- The portfolio remains fully invested with ~86.8% of the portfolio in small-cap stocks with the balance in mid-/large-cap stocks and cash.

- The portfolio continues to balance portfolio holdings between anti-fragile small- and mid-cap companies characterized by high cash-flow margins and high cash-flow yields, alongside those companies exhibiting accelerating business momentum.

- The three largest portfolio sectors at the end of the period were Information Technology, Industrials, and Financials.

- The three most recent additions to the portfolio were a U.S. post-acute healthcare company a two U.S. semiconductor companies.

- The three most recent exits were a U.S. professional services firm providing consulting and digital transformation services, a U.S. infrastructure and energy construction services company, and a U.S. specialty pharmaceutical company.

Navigator® SMID Cap Core U.S. Equity

- The portfolio remains fully invested with ~62.6% of the portfolio in small-cap stocks, ~32.3% in mid-cap stocks, and the balance in large-cap stocks and cash.

- The portfolio continues to balance portfolio holdings between anti-fragile small- and mid-cap companies characterized by high cash-flow margins and high cash-flow yields, alongside those companies exhibiting accelerating business momentum.

- The three largest portfolio sectors at the end of the period were Information Technology, Industrials, and Financials.

- The three most recent additions to the portfolio were the parent company of a U.S. grocery delivery and pickup platform, a U.S. medical device company, and a U.S. semiconductor company.

- The three most recent exits were a U.S. medical device company, a U.S. energy drink company, and a U.S. contract research organization.

Navigator® Taxable Fixed Income

- Within the portfolio, the focus remained consistent with previous months, keeping duration longer than the index and moving maturing and slightly longer bonds into the 5-year and longer portion of the yield curve.

- As rates moved higher throughout the month, duration was extended slightly longer than previous months to take advantage of the excess yield opportunities.

- This strategy of maximizing yield and extending duration will continue as long as interest rates remain elevated.

Navigator® Tax-Free Fixed Income

- The fact we enjoy positive returns in an environment where rates are squeezing higher is indicative of the importance of income and carry in our management mandate. We will continue to allocate a good portion of our investments to foundational, income-producing muni bonds.

- We think the yield curve has room to tighten more, and will remain cautiously incorporating moderate duration in the model without diluting the favorable convexity profile we have worked hard to achieve.

- We are actively navigating a diverging landscape in the state and city municipal bond market, making selective additions and reductions based on evolving fiscal conditions and credit rating changes.

Clark Capital’s Top-Down, Quantitative Strategies

May was an exceptional month for the markets, with the major indices closing the month at record highs. The S&P 500 has now advanced for nine consecutive weeks. The market has continued advancing as the fragile ceasefire in Iran holds with hopes of a negotiated settlement. Oil remains elevated, currently trading above $92.5/barrel, down from a high of $113.

Corporate earnings have powered ahead leading to an earnings driven bull market. In Q1, earnings grew by double digits for the sixth consecutive quarter, the longest streak since the earnings recovery following the global financial crisis. Earnings are now expected to grow by 24.3% this year and 15.7% next year. The outperformers are concentrated in Technology, semiconductors, and AI-adjacent themes, but the rising tide has lifted all boats, although not equally.

Our tactical models remain largely bullish. Fixed Income Total Return, Global Tactical, Global Risk Managed are all allocated risk-on. The Style Opportunity portfolio is overweight large caps, with an emphasis on large-cap growth.

Below are strategy updates from May:

Navigator® Alternative

- Managed futures have led performance in the portfolio’s mutual fund core, while multi-strategy funds have trailed.

- The portfolio moved into business development companies (BDCs) and listed private equity after their first quarter declines.

- More recently, we have reduced commodities and commodity equities in the belief that their price spikes will be temporary.

- We recently increased our positions in gold and gold miners as gold has corrected and appears to be holding at support.

Navigator® Fixed Income Total Return (MultiStrategy Fixed Income)

- By mid-May, the 10-year Treasury yield had risen 70 basis points since the war began, and historically high yield has fared well during times of rising rates.

- This time appears to be no different, as high yield spreads have narrowed to near all-time lows.

- Corporate earnings and fundamentals are not just healthy but robust, so our position in high yield should continue over the intermediate term.

Navigator® Global Risk Management

- Dynamic corporate earnings and fundamentals have also meant strong corporate credit, and our credit-based models have been strong and remain quite optimistic.

- We expect to continue our risk-on position over the intermediate-term.

- Resurgent U.S. technology stocks have returned U.S. stocks to leadership, but international equities are participating, if to a lesser extent.

- Cash would currently be our defensive vehicle of choice, but we don’t believe such a move is on the horizon.

Navigator® Global Tactical

- We maintain our bullish risk-on equity position that we established in early May 2025.

- Our credit-based models continue to signal a strong background for equities and risk assets, and surging corporate earnings have even kept multiples from rising.

- Though higher interest rates potentially create longer-term risks, so far, the strong economy has been able to overcome those headwinds.

Navigator® U.S. Sector Opportunity

- Only Technology and Materials rank above the S&P 500 in our relative strength rankings.

- Most subsectors of Technology are represented in the portfolio, including semiconductors, software, cloud, and cybersecurity.

- In the meantime, Energy has faded to near the bottom of our ranks after a performance spike. Health Care, Staples, and Consumer Discretionary are the weakest and to be avoided.

Navigator® U.S. Style Opportunity (MultiStrategy Equity)

- The portfolio focuses primarily on large-cap growth, which has surged over 28% and re-established leadership since the March market bottom.

- We continue to have a small position in mid-cap momentum, along with an over 70% indexed position.

- Large-cap value and lower beta factors rank lowest in our relative strength research.

Navigator® U.S. Strategic Beta

- The porfolio continues to modestly favor growth and beta while maintaining broad diversification.

- As 2026’s equity market rally has expanded, odds are growing that the portfolio will become more defensive in the coming months.

- We believe this year’s rally will eventually stall and undergo a correction, but such a correction would then represent another longer-term buying opportunity.

Disclosures

The views expressed are those of the author(s) and do not necessarily reflect the views of Clark Capital Management Group. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Clark Capital investments portfolio. Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies. For educational use only. This information is not intended to serve as investment advice. This material is not intended to be relied upon as a forecast or research. The investment or strategy discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances. Past performance does not guarantee future results. All investing involves risk, including the loss of principal, and there can be no guarantee investment objectives will be met.

Clark Capital Management Group (Clark) is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark’s investment advisory services can be found in its Form ADV Part 2 and/or Form CRS, which are available upon request.

Fixed income securities are subject to certain risks including, but not limited to: interest rate (changes in interest rates may cause a decline in market value of an investment), credit, payment, call (some bonds allow the issuer to call a bond for redemption before it matures), and extension (principal repayments may not occur as quickly as anticipated, causing the expected maturity of a security

to increase).

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and political and economic risks. These risks are enhanced in emerging market countries.

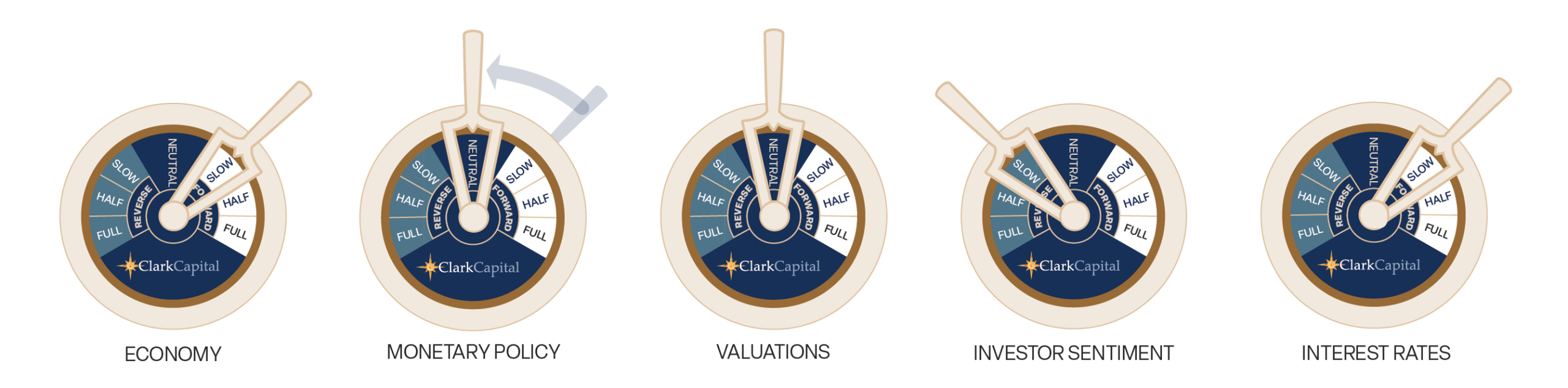

The “Economic Gauges” represent the firm’s expectations for the market, and how changes in the market will affect the strategy, but are only projections which assume certain economic conditions and industry developments and are subject to change without notice. For educational use only.

The S&P 500 measures the performance of the 500 leading companies in leading industries of the U.S. economy, capturing 75% of U.S. equities.

A 10-year Treasury note is a debt obligation issued by the U.S. Treasury Department that has a maturity of 10 years.

Treasury yield is the return on investment, expressed as a percentage, on the U.S. government’s debt obligations. Looked at another way, the Treasury yield is the effective interest rate that the U.S. government pays to borrow money for different lengths of time.

An AA bond rating signifies very high credit quality and a very low risk of default for a bond issued by a government or corporation, indicating a very strong ability to meet financial commitments that is not significantly vulnerable to foreseeable events. While not as exceptional as the highest AAA rating, an AA rating still provides strong reassurance to investors that their investment is secure.

An A rated bond signifies “high credit quality,” indicating a low risk of default, though it is more vulnerable to adverse economic conditions than higher-rated bonds. These ratings are issued by agencies like Fitch, S&P, and Moody’s, reflecting the issuer’s strong capacity to meet financial commitments, but with a greater potential risk than AA or AAA bonds.

A BBB-rated bond is an investment-grade bond that signifies an adequate, though not strong, capacity to meet financial commitments, carrying a low risk of default under normal conditions but a greater susceptibility to adverse economic or business factors compared to higher-rated bonds. In essence, these are considered the lowest tier of “safe” bonds before moving into the more speculative “junk” bond category.

The chartered financial analyst (CFA) charter is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income.

The Russell 1000 Value Index tracks companies with lower price-to-book ratios and lower expected and historical growth rates. Russell’s value indexes focus more on dividend yield.

The Russell 2000 Index measures the performance of the 2000 smallest U.S. companies based on total market capitalization in the Russell 3000, which represents approximately 10% of Russell 3000 total market capitalization.

The Bloomberg U.S. Corporate High-Yield Index covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. The S&P 500 and the Barclays U.S. Aggregate Bond Index are used as supplemental benchmarks.

The Bloomberg US Treasury Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint but are part of a separate Short Treasury Index. STRIPS are excluded from the index because their inclusion would result in double-counting. The US Treasury Index is a component of the US Aggregate, US Universal, Global Aggregate and Global Treasury Indices.

The MSCI All Country World ex USA Total Return (MSCI ACWI) is a market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. The MSCI ACWI is maintained by Morgan Stanley Capital International and is comprised of stocks from both developed and emerging markets.

ICE BofA US Corporate C Index, a subset of the ICE BofA US High Yield Master II Index, tracks the performance of US dollar denominated below investment grade rated corporate debt publicly issued in the US domestic market. This subset includes all securities with a given investment grade rating CCC or below.

Equity securities are subject to price fluctuation and possible loss of principal. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices. Certain investment strategies tend to increase the total risk of an investment (relative to the broader market). Strategies that concentrate their investments in limited sectors are more vulnerable to adverse market, economic, regulatory, political, or other developments affecting those sectors.